The electric trike for seniors in the UK is a small category today — and that is precisely the argument for it. Britain has the ageing curve of the Netherlands, the disposable income of Germany, and the older-adult cycling participation of neither: the UK ranks 25th in Europe for everyday cycling, and its over-70s cycle less than any other adult age group. Read that as a mature market and you’d walk away. Read it as what it actually is — structural unmet demand meeting a supply side nobody has organised — and you’re looking at one of the few genuine white-space windows left in European e-mobility. This article makes that case with UK data, then maps what a distributor or brand should do about it.

The three conclusions up front:

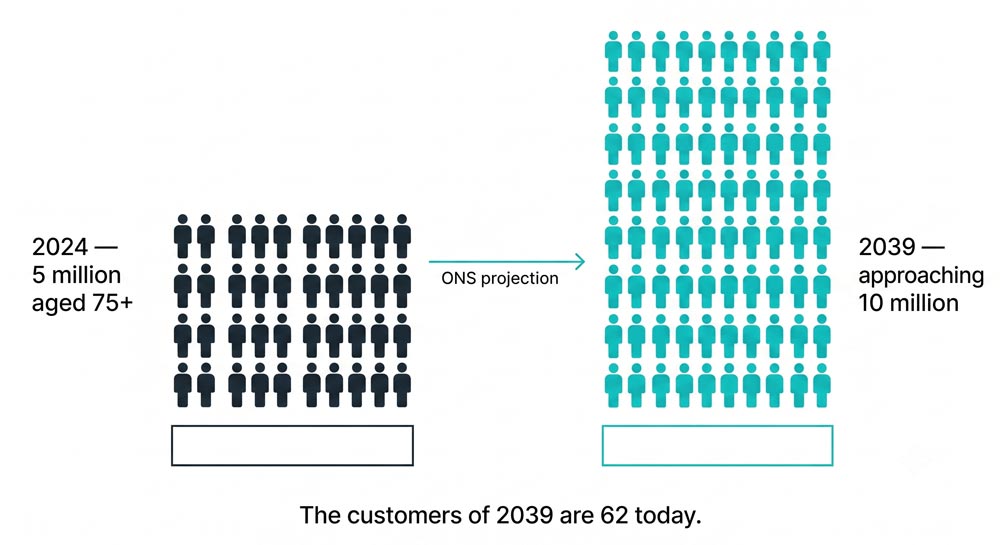

- The demand is demographically guaranteed. ONS projections — the most bankable forecast in British economics — put the over-75 population on course to double towards ten million by 2039. No market-sizing model in this industry rests on firmer ground.

- The low base is the opportunity, not the objection. British older adults don’t cycle less because they want to; the research shows they’re squeezed out by kit and conditions. Every percentage point of participation recovered is a new market, not a contested one.

- The window is open now and won’t stay open. The financial rails (VAT zero-rating, an uncapped Cycle to Work scheme), the demand infrastructure (inclusive cycling centres), and e-bike normalisation among older riders have all matured in the last five years — while dedicated supply hasn’t. That mismatch is the definition of a window.

How big is the senior electric trike market in the UK — and why is it growing now?

Honest answer first: today, it’s niche. Adapted-cycle retail is thin outside a handful of cities, and no reimbursement system ever built the category the way insurers built it on the continent. But market size is a snapshot; market direction is the investment case, and every UK-native indicator points the same way.

The demographics are not a forecast — they’re arithmetic.

In 2022, 19% of the UK population was aged 65 or over; the ONS projects that share rising towards 27%. The over-75 group — 5 million people — is on course to nearly double to 10 million by 2039, and the 85+ group to almost double by 2045. The people who will be 75 in 2039 are 62 today. They are this category’s customers, and they already exist.

The silver pound is real and increasingly active.

Britain’s over-65s hold a disproportionate share of household wealth, and the spending pattern of the newly retired has shifted decisively towards leisure, health and staying active — the exact use-case cluster this vehicle serves: the towpath ride, the pop to the shops, the allotment run, the grandchildren’s school gate.

Adaptive demand is already hiding inside the e-bike boom.

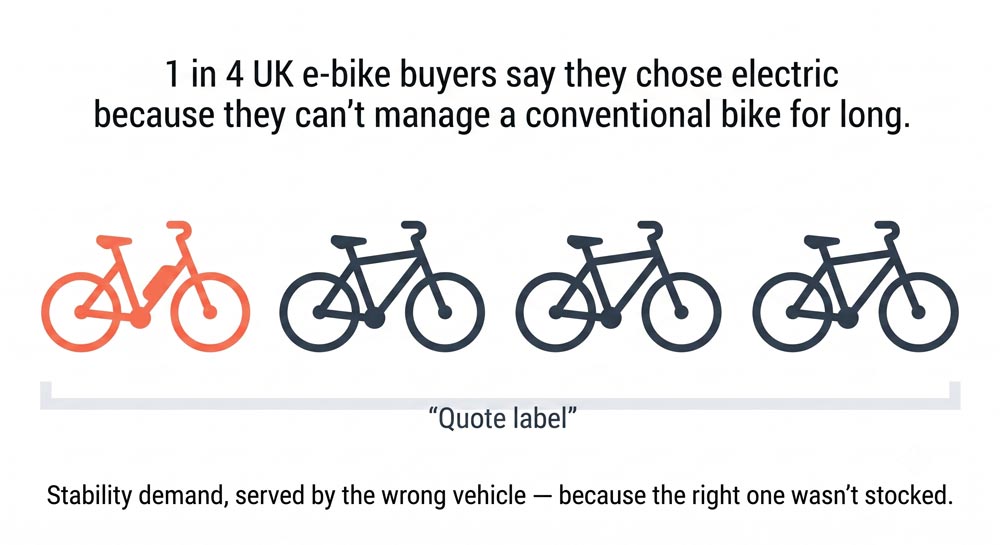

In UK purchase-motivation research, 54% of e-bike buyers cite “less effort than a conventional bike” and — the number that matters — a quarter say they bought one because they can’t ride a conventional bike for long. That is stability-and-stamina demand being served by a two-wheeler because the three-wheeled option isn’t on the shop floor. The customer walked in; the category wasn’t stocked.

Why do older people stop cycling in the UK? (The answer is the opportunity)

Here’s the puzzle worth an investor’s attention. In the Netherlands, the over-65s cycle for a higher share of their trips than almost any other adult age group. In Britain, cycling participation drops off a cliff past 70. Same physiology, same climate band — wildly different outcome.

UK transport research gives the uncomfortable explanation: even where British cycling has grown, the representation of older adults in that growth has fallen. The barrier isn’t desire; it’s fit. Traffic-mixed roads, a fitness-flavoured cycling culture built around drop-bar sport rather than everyday utility, and — critically — a vehicle format that demands the balance and confidence of a forty-year-old. British older adults haven’t rejected cycling. They’ve been priced out of it in confidence terms.

That’s what makes the low base bullish. The Dutch figure isn’t a cultural quirk; it’s proof of what participation looks like when the vehicle and environment fit the rider. And the UK environment half is finally moving: a national network of inclusive cycling centres now puts older and disabled riders on adapted cycles every week in safe, traffic-free settings — free demand generation at national scale, funded by the third sector. What the movement itself admits is that the step after the try-out barely exists: sparse dealers, long waits on continental imports, prices set for insurance-funded markets. Demand is being manufactured faster than supply. That gap is the business.

Is there government funding for electric trikes in the UK?

There’s no NHS prescription and no council grant — Motability, the UK’s flagship mobility scheme, covers cars, scooters and powered wheelchairs but no cycles at all. What exists instead are three financial rails, and every one of them is administered by the trade, which is exactly why the trade should learn them cold:

VAT zero-rating — the 20% lever.

Cycles designed solely for use by disabled people can be sold VAT-free to eligible customers, who self-declare at the till on a one-page form. The catch sits on the product side: “designed solely” is a design-and-documentation test, and HMRC’s guidance for recumbent formats is acknowledged in the sector to be unclear. A generic leisure trike with a marketing sticker won’t survive scrutiny; a genuinely accessibility-engineered platform with a design dossier has a case. Whoever holds that dossier hands their dealers an automatic 20% price advantage.

Cycle to Work — the uncapped rail.

Since the £1,000 ceiling went in 2019, salary sacrifice covers e-cycles and adapted cycles at realistic price points, saving 32–47%. The senior angle is under-exploited: with the State Pension age at 67 and rising, the 60–67 stability-conscious buyer is still on a payroll — inside the scheme’s reach and invisible to continental incumbents who never had to think about employer channels.

Access to Work — the grant nobody merchandises.

Where a cycle enables a disabled person to work, Access to Work has funded it. Volumes are modest; the customers are fully funded, and a one-page dealer guide to the application is the cheapest differentiation in this market.

One legal note that closes the sale for the active buyer: an e-trike meeting the EAPC rules — 250 W maximum continuous power, assistance cutting out at 15.5 mph, rider 14+ — is legally a bicycle. No licence, no registration, no insurance, full access to cycle lanes. A mobility scooter is capped at walking-to-jogging pace, banned from cycle infrastructure, and announces something a trike doesn’t.

What should a distributor look for in a senior electric trike for the UK?

The UK brief differs from the continental one in ways a spec sheet either respects or doesn’t:

- Torque before top speed. Assistance is capped at 15.5 mph everywhere, but Britain has hills the Netherlands doesn’t. The number that matters is pulling away uphill from a standstill with no balance moment — which is why the 120 N·m mid-drive in the UM Chill spends its headroom exactly where UK riders need it.

- A shed test, not a showroom test. Terraced-house storage, caravan holidays and driving-to-the-ride club culture all reward a compact or modular frame. The UM Vita‘s transportable footprint answers the question UK dealers report hearing first: “will it go in the shed, the caravan, the boot?”

- Weather-readiness as a credibility signal. Full mudguards, sealed electrics, corrosion-resistant fasteners, puncture-resistant tyres. Not premium options — proof the product was specified by someone who’s seen a British February.

- De-medicalised design. The UK buyer this article describes has never been near an assessment. City-bike design language is what lets a dealer sell to a 63-year-old who “doesn’t need one of those yet”.

Why the manufacturer decides whether you can compete

Look back over this list — the VAT design dossier, EAPC-conformant drive configuration, documented step-in geometry, UK-spec weatherising, torque tuning — and notice that not one item can be fixed downstream. Every advantage in the UK’s open market is created or forfeited at the factory.

This is where senior mobility stops being a product category and becomes an engineering discipline — and it’s the discipline United Mobility has spent nearly two decades practising. A step-through frame and a basket do not make a vehicle senior-ready. Our Vita og Chill semi-recumbent platforms are engineered as documented accessibility products: seated step-in entry designed around the balance moment where older riders actually come off, measurable ergonomic data (seat height, step-in clearance, boarding angle) your dealers can quote, EN 15194 conformity, and per-market ODM configuration — UK drive settings, weather packages, branding and finishing to your range plan.

The UK window rewards whoever arrives first with a credible product, because there’s no regulatory queue to hide behind — and none to be protected by. If Britain is on your roadmap as a distributor, an inclusive-mobility retailer, or an e-bike brand extending into stability products, brief our engineering team on your channel plan — and take our manufacturer evaluation checklist with you when you compare us against anyone else.

Next in this series: Denmark — where the public system grants mobility scooters instead of trikes, in the world’s second cycling nation.

FAQ

How big is the senior electric trike market in the UK?

Small today and structurally set to grow: the ONS projects the over-75 population to nearly double towards 10 million by 2039, UK e-bike purchase data already shows a quarter of buyers choosing electric because they can’t manage a conventional bike for long, and dedicated adapted-cycle retail remains sparse. Low base, hard demand drivers, thin supply — the profile of a growth window rather than a mature niche.

Is there any government funding for an electric trike for seniors in the UK?

No NHS or council reimbursement, and Motability excludes cycles. Three retail-side mechanisms exist: VAT zero-rating for cycles designed solely for disabled people (customer self-declares at purchase), the Cycle to Work salary-sacrifice scheme (uncapped since 2019), and Access to Work grants where a cycle enables employment.

Do you need a licence or insurance for an electric trike in the UK?

No — provided it meets the EAPC rules: 250 W maximum continuous power, assistance cutting out at 15.5 mph, rider aged 14 or over. It’s then legally a bicycle with full access to cycle lanes and paths.

Why do so few older people cycle in the UK compared with the Netherlands?

UK research points to fit, not desire: traffic-mixed roads, a sport-flavoured cycling culture, and vehicle formats that demand young-adult balance. Where the environment and vehicle fit the rider — as in the Netherlands — over-65s cycle as much as any adult group. Closing that gap is precisely what the adapted e-trike category exists to do.

What makes a manufacturer credible for the UK senior e-trike market?

Documented accessibility engineering (it underpins the VAT zero-rating case), EAPC/EN 15194 conformity, UK-appropriate torque and weatherproofing, and ODM capacity to configure per market. United Mobility builds its Vita and Chill semi-recumbent platforms to exactly this brief, with the ergonomic documentation dealers and advisers can quote.